DeFi 2.0: An Upgrade to the First Generation of DeFi

This article covers the fundamentals of Defi 2.0 while discovering the need for DeFi 1.0 evolution.

Several crypto users are getting weary of DeFi 1.0 due to its many flaws and inconsistencies. To newbies, these flaws are not obvious, but to oldies, these flaws are very obvious. All of the flaws associated with DeFi 1.0 are due to its instability and lack of popular acceptance.

Seeing that DeFi 1.0 can’t match the pace of crypto advancement, there is a need to launch into a better crypto world. Hence, the essence for the creation of DeFi 2.0.

DeFi 2.0 is an advanced version of the DeFi 1.0 with several improvements and addition to its networking. As a trader, we’ll recommend that you know so much about this new system network.

In this article, we’ll be discussing DeFi 2.0 in detail and the problems it will be solving. Also, we’ll be discussing how DeFi 2.0 solves these problems and why it is better than DeFi 1.0.

What is DeFi 2.0?

The DeFi 2.0 is an advancement of the DeFi 1.0 with improvement on its liquidity infrastructure layer and sustainability of the Decentralized Financing project.

DeFi 1.0 offered users liquidity mining, AMMs, lending, and token exchange. The DeFi 1.0 network was also offered alongside many projects that made transactions on the ecosystem comfortable and secured. Some of these projects are

Although these projects were incredible, there had to be improvements on the DeFi 1.0 ecosystem to accommodate the newly developed projects. The DeFi 2.0 will offer everything DeFi 1.0 will offer and many more. That is, the DeFi 2.0 ecosystem will offer liquidity, AMMs, lending, token exchanges, new finance technologies, user experience, and some improvement to capital utilization.

To improve on the capital utilization and use experience, DeFi 2.0 will be solving problems DeFi 1.0 couldn’t solve.

Meanwhile, here are some drawbacks to DeFi 1.0

So far. DeFi 1.0 has not been able to form close connections between its users. It forms weak vertical links and horizontal connections. To worsen it all, DeFi 1.0 is responsible for the cold transactions that occur on the website.

DeFi 1.0 didn’t focus on decentralized finances. It allowed transactions based on interest and enthusiasm. So, authorization of transactions was assigned to only specific individuals on the network.

A major disadvantage of the DeFi 1.0 was its means of accruing funds for transactions. It is used to acquire funds to loans via deposits from depositors for deposit claimers. This means of funding loans became a big problem over time. Hence, a need to find other alternatives of funding liquidity pools for loans.

These said, just like DeFi 1.0, DeFi 2.0 will come alongside various, better, and more problem-solving projects too. Some of these projects are:

The Olympus DAO serves to solve one of the biggest problems with DeFi 1.0. DeFi 1.0 was DeFicient in how it sourced funds for loans. It focused majorly on using funds from users to supply its bridge pool.

It'll mean that if there is no supply from users, there won't be a supply of funds to the bridge pool. Consequently, there won't be loaning in the network.

To properly handle this, Olympus DAO will be sorting funds for bridge pools without getting any from users. This is why Olympus DAO is often referred to as the alternative model to liquidity mining.

Olympus DAO is an algorithmic protocol that utilizes bond mechanisms to help it serve as an alternative for liquidity mining. It's the first protocol to use this kind of liquidity mining mechanism.

Olympus DAO can function effectively by issuing its tokens at lower costs for easy purchase. With this, the OHM (Olympus DAO Token), will be able to secure a position in the market to create protocol-owned liquidity.

Each OHM is oftentimes backed by DAI. It means that one OHM is backed by 1 DAI. So, higher OHM prices will mean more DAI pumped into the pledge contract. Consequently, more returns are available during participation in OHM pledges.

With this mechanism, the price of OHM is constantly maintained above 1 DAI and the market cap steadily approaches the overall asset value of Olympus treasury.

In addition to all these said about the Olympus DAO, we must mention that users don't own the tokens on this system; it is the protocol that owns the tokens.

This is an advantage as it helps to prevent selling pressure from immediate liquidity providers. So, it is Olympus DAO filling in the place of liquidity providers.

Abracadabra

Abracadabra works like MakerDAO in that they both are lending platforms and collateralize users’ assets to generate stable coins. Also, they both function by using protocol incentive tokens.

But unlike MakerDAO, Abracadabra collateralizes assets with proceeds such that users can use tokens to mint or borrow stable coins some of the tokens Abracadabra uses are yvUSDT and xSUSHI being tokens. By using these tokens, they can free up assets, liquidity, and user revenue.

Abracadabra has lending advantages too and some of them are:

Abracadabra offers a very low cost of borrowing and low, stable interest rates

Independent liquidity risk with no linkage to other collateral.

Conversion of assets with high potential of yielding interest into liquidity for the increment of income and capital leverage.

On the whole, Abracadabra enhances the utilization of funds and reduces the chances of liquidation.

Convex Finance

Convex finance has embarked on the journey to improve the user experience in DeFi 2.0. It will be doing this by showcasing a one-stop platform for its users for liquidity mining and CRV pledging.

In the end, convex finance will be developing the CRV ecosystem by balancing CVX tokens by simplifying the CRVA locking, pledging, and process of the curve.

Recent breakthrough with DeFi 2.0

One of the key indicators of the growth of DeFi 2.0 is the quick growth of its projects on the ecosystem. So far, Convex finances a Total Value Locked {TVL} of 14.55 billion surpassing yearn of .0 billion.

In the same way, Abracadabra has accrued 4.2 million and Olympus DAO accruing 650 million growth change. All of these are clear indicators of the effectiveness and efficiency of DeFi 2.0.

Which Way to Go?

We have seen the differences between the two DeFis, weighing their cons and pros, and have submitted our resolution to you to pick which best suits you.

No one will prefer DeFi 1.0 over DeFi 2.0 seeing its ease of adaptability and its ease of incorporating ability into several crypto networks. You may want to deny it but several applications and transactions will soon wear out your patience for DeFi 1.0.

Instead of sticking to the old man, why not launch into newer experiences and enjoy smooth transactions on DeFi 2.0?

Serum: A Blend of Speed, Convenience and Trustlessness

As the next-generation exchange system, Serum is making waves in proving its credibility in crypto-trading and decentralized finance transactions. It provides faster and frictionless orders with its automated order book system.

Serum provides incentives to its users which in turn favors so many developers. Some of these incentives are Serum Token (SRM) and MegaSerum Tokens(MSRM). With these tokens, one can achieve passive crypto income by staking their tokens on Serum.

Serum allows every member to stake their tokens. It doesn't only allow members with the highest token to stake, it also allows members with small tokens to stake too.

Seeing that Serum DEX has so much to offer, there's a need to know so much about it. In this article, we'll extensively discuss Serum DEX and its features. Also, we'll discuss the values and how it relates to other blockchains. Enjoy!

What is Serum?

The Serum is a decentralized exchange system built on the Solana ecosystem to provide unmatched low costs and speedy DeFi transactions. It charges as low as 0.0001 cents for transactions.

The system aims to offer users faster settlement times and zero centralization.

In offering a non-centralized side of its architecture, it centralizes price fees even without using Oracles services. Hence, we say the Serum system functions without Oracles. Oracle is a centralized service used by Defi protocols to verify, authenticate and query external data then send them to an already closed system.

Because Serum is based on the Solana blockchain, it offers fully decentralized services that are easy, fast, and affordable to use.

In Serum DEX, users can easily transfer assets amongst different blockchains and even trade stable coins and wrapped coins or even convert coins from one coin to another. For instance, converting Ethereum to FxT. Some of the projects build on Serum DEX are:

Furthermore, users can create customized financial products as they deem fit.

The Serum uses native Serum tokens(SRM) as its main governing assets and incentive for its ecosystem. With SRM, users can stake, trade, or participate in burn and buy fee incentives for reduced trading costs.

Also, with the SRM, users enjoy a further reduction in Serum-based transactions.

Aside from all of these, Serum aims to enhance frictionless cross-chain contracts in DeFi while traders trade synthetic assets. It provides many synergies with the Solana blockchain serving as its host application.

Solana Blockchain

As the fast-growing blockchain system, Solana has secured a spot in the top 10 cryptocurrency projects according to the market cap. Being able to carry out fifty thousand transactions in a second(TPS), Solana blockchain has demonstrated to be the quickest blockchain anywhere on the globe. So, Serum building their project on the Solana network will allow for quick fast transactions on the Serum network.

Solana, with all of its functions, is a layer-1 blockchain. So, to function effectively, Serum functions solely on a layer-1 solution system without layer-2 solutions. It operates solely on a decentralized clock that monitors time-stamps transactions together with an advanced Proof-of-Stake(POS) mechanism.

In recent times, blockchain developers have been designing decentralized applications using the Solana blockchain. This widely accepted choice from blockchain developers is due to Solana's reputation in providing fast and scalable smart-contract-enabled blockchain. It's this advanced blockchain system that the Serum network is built on. Clearly, Serum is just a project on the Solana ecosystem.

That said, Serum DEX mirrors the cost and speed of the Solana network. With this, it offers a fully decentralized trading arena with easy trading on centralized exchange systems. It also offers inter-operable features that allow users to exchange assets such as Ethereum (ETH), Bitcoins (BTC), SPL-based tokens, and ERC-based Tokens.

Serum Token (SRM)

A unique thing about the Serum token (SRM) is its means of collecting values. It accrues values via hyperinflation.

SRM accrues values through adoption and utility. Some are:

All Serum's net fees go to burn.

50% off on all Serum fees on holding a token.

Fees payment with SRM.

That said, most SRM have extensive unlocking terms with all sales fees inclusive. Serum achieves this by locking the tokens. SRM are locked cryptographically in a smart contract. It takes about a year or less to unlock a locked token.

The period where you cannot unlock a locked token is its unlocking period. Most SRM have an unlocking period of one year.

In some cases, some SRM take up to 6 years to unlock. This type equates to 1/2190 SRM in a day.

SRM amount to a maximum of 10 Million tokens, creating about 175 million tokens in its circulation. Because of this high number of tokens in circulation, Serum has been able to provide liquidity to their project. However, several token stakeholders have decided to hold on to a large number of their tokens thereby reducing the number of tokens in circulation.

Moving on, several traders stake SRM to achieve passive crypto income. They also do this by rescuing fees and staking rewards when trading on Serum DEX.

Howbeit, traders with SRM can still partake in on-chain governance. Traders who do this will vote on updates to specific markets on the project.

MegaSerum Tokens (MSRM)

A MegaSerum(MSRM) is equivalent to one million SRM. It means you have to have a million SRM as they'll amount to one MSRM.

MegaSerums are rare and there are only 10%. This is so as there are just fewer users that show belief and commitment to the Serum network. It's just those 10% that can lock their SRM with MSRM.

Project Serum Cryptocurrency Ecosystem

The project Serum, built on the Solana ecosystem, provides usable services to developers and other users from the start of their project to its deployment. On a large scale, this ecosystem provides a suitable platform for non-technical users planning on delving into Decentralized Finance(Defi). This they can do on Serum's user-friendly App(dApp).

That said, in the Serum ecosystem, developers are automatically eligible for grants once they build on this network. With this, projects receive the support and funding to enhance their user adoption and brand awareness.

A good example of a project like this is the Phantom project. The Phantom project is a Defi(Decentralized finance) and NFT crypto wallet. Another example is Coin98 that offers users smooth running payment gateway services.

Also, Project Serum provides developers contact points and resources. With that, you can view on-chain codes, clients codes, and repositories. The project also offers tutorials for developers which can be found on the "Developer Resources" on its website.

Finally, the Project Serum allows users to comprehensively overview all Serum's tokens and integration within its ecosystem. And to top it all, the project provides a link to its whitepaper.

Serum and Staking Nodes

Before one becomes a Serum node, one must take at least 10million SRM including a minimum of 1 MSRM. However, at 100 million SRM or 100 MSRM tokens, nodes stop staking tokens.

Nodes collect several rewards based on their network participation, the aggregate of activity, and performance within the Serum ecosystem. Generally, nodes are in charge of some blockchain operations like cross-chain settlement validation.

Staking

Oftentimes, traders can't continue the Serum project and earn passive income via Defi because they can't stake 10 million Serum tokens. This shouldn't be a challenge as there are alternatives to this.

Serum token holders can now stake tokens as regards a node. A node is formed by a leader and consists of members of that network. The node leader doesn't necessarily have the highest tokens. But the leader can be the founder of the node and will receive small fractions of node staking fees.

In a node, anyone or the leader can stake a node on behalf of another member. Still, Serum nodes will offer trading fees and governance rights within its ecosystem.

However, there're mechanisms to provide an overload of tokens in the ecosystem. As many readers stake their SRM tokens, the system cools down following unstacking tokens. This period, known for just a week.

Node Rewards

In a node, rewards are distributed through native SRM. However, the nodal leaders receive more proportion of the node than other members. Commonly, the leader receives 15% of the rewards while the 85% is distributed among other members.

Annually, nodes receive a 2% percentage yield (APY) based on their staked funds. However, this percentage can increase to around 13%. This can only be possible if members of a node increase their performance duties and challenges. Also, nodes get special rewards for special challenges. One of these challenges includes providing collateral for SRM tokens. The aim of this is to prevent funds from burning.

How to Use Serum

Serum exchange doesn't require that users own an account before a transaction. All you need to transact on Serum DEX is an internet connection, a wallet, and some cryptocurrencies.

First, if you're carrying out a transaction on Serum, you’ll be needing a Solana wallet. Asides from the Solana wallet, there are other wallets that Serum interacts with.

To switch between the wallet, click on the change wallet at the top right corner of the interface. Then pick your desired wallet.

Here is a breakdown of how to use the Serum before we delve into each process extensively.

Create a Solana wallet

Here is a link that explains how to create a Solana wallet.

After creating a Solana wallet, on the first opening, you’ll be asked to write down your recovery keys. Make sure to write them somewhere first as you’ll be needing them some other time.

Often, we advise users to create a password immediately after creating their Solana wallet.

After creating a password, you’ll be asked to re-enter your new password for confirmation.

After doing this, you click on continue. There you have it. You have just created your Solana wallet.

On your Solana wallet, you can deposit Eth and convert it to Sol and vice versa. As you’ll expect, there are conversion fees associated with this.

From another exchange system, you can click on the cryptocurrencies you have there and transfer them to your Solana wallet. In withdrawing your cryptocurrencies, you’ll be needing your already copied Solana wallet link to be able to receive your money.

To successfully withdraw, you will need to authenticate your transactions.

After a complete authentication, you can head to your Solana wallet. It’s critical to mention that this transaction doesn’t take long. It only takes a maximum of two minutes to complete a transaction.

Seeing that your cryptocurrency has arrived in your Solana wallet, you can add tokens by clicking on the add token feature on the interface. One may choose to add Serum unwrapped Bitcoin to the Sol.

These wrapped tokens can then be in the deposit and become real underlying assets.

Also important to note is the small fee attached to adding tokens to a Solana wallet.

The next thing to do is to find a Serum-based DEX to connect to this wallet.

Connecting your Wallet to Serum DEX

Connecting your wallet to Serum DEX shouldn’t be challenging provided you follow these easy steps. Below are simple steps on wallet connection.

On the Serum DEX interface, click on "connect" on the top right corner of the interface.

Ensure you must have selected your desired wallet before clicking connect.

And if you wish to change your wallet, you must disconnect from the current wallet, then, you can click the select wallet feature to pick your new wallet.

The Value of Serum

As of the time of writing this article, Serum values was the 11th most trending cryptocurrency. On the other hand, it was 141st on the coin market cap on that same day.

Serum DEX offers a platform for developers and other users to trade speedily and conveniently. For developers, it provides contact points and resources. Such that, they can view on-chain codes and attend tutorials. All that Serum offers is because of its conjunction with the Solana network.

Today, lending is one of the most important financial activities in society. It fuels economic growth and facilitates commercial activities. The size of the world’s debt markets as of 2020 was estimated to be more than $281 trillion, more than three times the world’s annual output. This paper focuses on DeFi lending markets being created through the use of blockchain technology.

Traditional Lending and its Problems

Credit, offered by a lender to a borrower, is one of the most common forms of lending. Credit fundamentally enables a borrower to purchase goods or services while effectively paying later. Once a loan is granted, the borrower starts to accrue interest at the borrowing rate that both parties agree on in advance.

When the loan is due, the borrower is required to repay the loan plus the accrued interests. The lender bears the risk that a borrower may fail to repay a loan on time (i.e., the borrower defaults on the debt). To mitigate such risk, a lender, for example, a bank, typically decides whether to grant a loan to a borrower based on the creditworthiness of this borrower, or mitigates this risk through taking collateral - shares, assets, or other forms of recourse to assets with tangible value. Creditworthiness is a measurement or estimate of the repaying capability of a borrower . It is generally calculated from, for example, the repayment history and earning income, if it is a personal loan.

The current mainstream lending market, led by banking institutions, is fraught with issues as highlighted below.

Financial Exclusion

Individuals or entities with thin credit files face financial exclusion from present lending institutions, which have stringent lending rules and underwriting models to reduce default risk. The International Finance Corporation estimates that 65 million firms have unmet financing needs of $5.2 trillion each year.

Liquidity inefficiency

The supply and demand side of lending is fragmented based on lending period, interest rate, credit rating etc. in the present markets. This results in sub optimal liquidity. Further, the oversupply of liquidity in one submarket cannot be promptly transferred to serve the demand of another submarket.

Subprime problems

The financial exclusion in current systems has given rise to alternative lending entities, including peer-to-peer lending markets. These lending entities typically charge borrowers a premium for securing funding, understanding that the borrowers are left with no other options to source funds. Because these markets are non-regulated, fraudulent activities and high default rates permeate these less strict lending markets.

During 2007 financial crises, institutions were left holding trillions of dollars worth of near-worthless investments in subprime mortgages.

Legacy infrastructure

The dated information technology infrastructure used by mainstream lending entities is a crucial impediment to efficiency and speed. There is limited data exchange between financial institutions. Credit history and other related information is fragmented and opaque.

Key Concepts in DeFi Lending

Despite their respective distinctions, most DeFi lending protocols share two features; they have replaced centralised credit assessment to codified collateral evaluation, and they employ smart contracts to manage the system functionalities. Some key concepts being used by most DeFi protocols are highlighted below.

Value locked

Value locked represents the total users’ deposits in a protocol’s smart contracts. The locked value serves as a collateral or reserve to back the system.

IOU token

Lending protocols issue users IOU (I Owe You) tokens against their collateral deposits. These IOU tokens redeem deposits at a later stage, and they are also transferable and usually tradeable in exchanges.

Collateral

A loan’s collateral represents the entirety or part of the borrower’s deposit against the loan. The collateral ratio determines how much loan a user is allowed to borrow.

Liquidation

The liquidation of a loan is triggered automatically by a smart contract. When a loan’s collateral ratio drops below a critical threshold due to interest accrued or market movements, any network participant can trigger the function to liquidate the collateral.

Interest Rates

Borrowing and lending interest rates are computed and adjusted by smart contracts according to the supply-borrow dynamics, based on protocol-specific interest rate models.

Yield

The total amount of profit or income produced from a business or investment is referred to as yield. In DeFi, it is often measured in terms of Annual Percentage Yield (APY). Yield is relevant to the suppliers of loans, and is largely dependent on borrowing demand.

Key Architecture Elements

Oracles

The market price information of locked and borrowed assets are supplied to smart contracts through external data feeds providers called “price oracles”. An oracle imports off-chain data into the blockchain so that it is readable by smart contracts. There are different kinds of oracles that the lending borrowing protocols use. Such as, chainlink or any custom made DEX oracles such as uniswap’s TWAP.

Lending pools

Liquidity pools are markets of loans for crypto-assets. Users called liquidity providers (LP), act as lenders and supply an asset to the protocol. In return, they receive a claim to the supplied asset represented as minted tokens (IOU). In return for liquidity provision or supplying assets, lenders are given incentive in the form of interest. At any time, lenders can redeem their IOUs by transferring minted IOU tokens to the protocol, which then pays back the original tokens (with accrued interest) to the redeemer, simultaneously burning the minted tokens (IOUs). This can be seen by a simple representation of providing liquidity on Compound protocol shown below. A user supplies ETH as an asset and gets cETH as an IOU token, which can be redeemed back for the underlying ETH plus interest paid in the units of supplied asset, in this case ETH.

Borrowers can initiate a loan by borrowing tokens deposited in a pool. This can be seen by a simple representation of borrowing on Compound protocol shown below in which a user deposits ETH as collateral and gets cETH as an IOU token representing the collateral plus the borrowed DAI. The collateral can be redeemed by paying back the borrowed amount plus the interest. The interest rates paid and received by borrowers and lenders are determined by the supply and demand of each crypto asset. Interest rates are generated with every block mined.

To ensure that borrowers eventually repay the loan, they are required to provide a collateral (usually in the form of ETH). An unpaid loan of person A can be liquidated by person B, who pays (part of) A’s loan in return for a discounted amount of A’s collateral. For this to be possible, the value of the collateral must be greater than that of the loan. To illustrate this, let's say a borrower has taken out a loan of 100 DAI by depositing $150 worth of ETH as collateral, given that the required collateralization ratio is 150%. If ETH falls in value and if the borrower’s collateral is now worth less than $150, then anyone can pay for the loan by paying 100 DAI for the loan, and in return can get the ETH deposited by the borrower as collateral at a discounted rate set by the protocol.

Tokens

In DeFi, tokens can represent a user’s share in a liquidity pool or serve the purpose of keeping the markets in equilibrium and to ensure that all actors behave honestly. Protocols also distribute governance tokens that allow holders to propose and vote on protocol changes, such as modification of interest rate models. Governance tokens are often given as a reward to incentivise participation, from both borrowing and lending sides, in a protocol. One more usage of governance tokens from the perspective of a protocol is to pay debt in the scenario of a black swan event.

Key Participants

Lender and Borrowers

They are the main users of the protocol. Lenders supply assets for loans in order to earn yield or interest income from their holdings. Borrowers on the other hand, take loans to get liquidity by providing collateral. They do this because they expect appreciation in the price of their collateral and don’t want to sell it to access liquidity. The loan can be used for consumption, allowing the person to overcome a temporary liquidity squeeze or to acquire additional crypto assets for leverage exposure.

Keepers

Protocols may require that the on-chain state is continually updated to maintain certain standards such as collateral ratio. To trigger state updates, certain protocols rely on external entities called Keepers. Keepers are generally financially incentivized to trigger such state updates. For instance, if a protocol requires a user’s collateral to be automatically liquidated under certain conditions, the protocol will incentivize Keepers to call transactions to trigger such liquidation and in return the Keeper will receive the liquidated collateral at a discounted price. The network of Keepers can be based on pure P2P execution or a consortium based on some consensus protocol such as PoA, or PoS.

Governance

Governance, in DeFi, is the process through which a protocol is able to make changes to the parameters which establish the terms of interaction among participants. Such changes can be performed either algorithmically or by agents. Presently, a common approach to governance is for a protocol to be initiated with a foundation. The foundation has control over governance parameters, with a promise to eventually decentralize its governance process in future. Such decentralization of the governance process is instantiated through the issuance of a governance token, an ERC-20 token which entitles token holders to participate in protocol relative to their share of total supply. Governance can be both full on-chain, off-chain or a hybrid combination of both.

Basic coin voting can empower large whales to vote on the system and virtually hijack it. But this can be mitigated through Quadratic voting. Detailed information on the topic of DeGov can be found here.

Types of DeFi Lending Approaches

Protocols in DeFi follow different approaches for lending: Collateralized debt positions, P2P collateralized debt markets, Under collateralized borrowing and Flash loans.

Collateralized Debt Positions

Contrary to the traditional lending markets, the lack of a creditworthiness system and enforcement tools on defaults leads to the necessity of overcollateralization in most lending and borrowing protocols (e.g. Compound, Aave). Over-collateralization means that a borrower is required to provide collateral that is higher in value compared to the debt being taken out. To maintain the over-collateralization status of all the borrowing positions, lending pools need to fetch the prices of cryptocurrencies from price oracles.

Once a borrowing position has insufficient collateral to secure its debts, liquidators are allowed to secure this position through liquidations. Liquidation is the process of a liquidator repaying outstanding debts of a position and, in return, receiving the collateral of the position at a discounted price. At the time of writing, there are two dominant DeFi liquidation mechanisms. One is the fixed spread liquidation, which can be completed in one blockchain transaction, while the other one is based on auctions that require interactions within multiple transactions.

To illustrate the concept, let's take the example of Compound protocol. Users of Compound can lend and borrow ETH and other ERC-20 tokens. Users who lend their token receive IOUs in the form of cToken (e.g. cETH, cDAI) of an equivalent value in return. The IOUs can be used to redeem the supplied asset by the lender and accrue the interest. The deposits of all lenders are pooled together and they start earning interest right when they deposit their funds in the smart contract based pool. However, the interest rates are dependent on the pool’s utilization rate. When liquidity supply is high loans will be cheap as interest rates will be lower. When loans are in demand, borrowing will become more expensive with interest rates becoming higher.

Lending pools have the additional advantage that they can maintain relatively high liquidity for the individual lender in case of redemption. The role of the keepers comes into play in the CDPs liquidation process.

P2P collateralized debt markets

This approach works by matching lenders with borrowers. In other words, for someone to be able to borrow ETH, there must be another person willing to lend ETH. Loans are collateralized in this approach too in order to mitigate counterparty risk and to protect the lender, the collateral is locked in a smart contract. Under this approach, the lenders do not automatically start earning interest, but only once there is a match with a borrower. The advantage of this approach is that the lenders and borrowers can specify terms of loan such as time period and fixed interest rates.

From a technical perspective, a state channel can be opened between both parties with the signature verification done on the base chain. And the channel will be closed only if both parties agree that settlement has been done correctly.

Under-collateralized

Under-collateralized borrowing also exists in DeFi (e.g. AlphaHomora), however in a limited and restricted manner. A borrower is allowed to borrow assets exceeding the collateral in value, however, the loan remains in control of the lending pool and can only be put in restricted usages (normally through the smart contracts deployed upfront by the lending pool). For example, the lending pool can deposit the borrowed funds into a profit generating platform (e.g. Curve ) on behalf of the borrower.

Flash Loans

An alternative to over-collateralized loans are flash loans. Flash loans take advantage of the atomicity of blockchain transactions. Atomicity means that multiple actions can be executed within a single transaction. Even if one of the actions is not executed, the whole transaction is reverted. Because flash loans are taken out only for the duration of a single transaction, they allow the borrower to take out loans and repay the full borrowed amount plus fees by the end of a single transaction. Aave is one of the first protocols that supports “flash loans”, later on followed by Uniswap.

DeFi Lending Snapshot

We can see from the chart below that the Total Value Locked (TVL) in DeFi lending has meteorically increased over the last year rising from almost $4B to $39B, posting an increase of almost 10X.

In terms of protocols with highest TVL, Aave tops the list with a current share of approx. 37.5% followed by Compound (25%) and Maker (21.8%). InstaDapp is a lending aggregator, hence we do not account for it here as this could result in double counting the TVL. The combined TVL of the 3 highlighted platforms constitutes approx. 85% of the entire DeFi lending TVL which shows their dominance.

Interest Per Year (IPY) is the speed at which interest is accruing in DeFi. IPY is calculated by multiplying the current borrow rate by the total outstanding debt. The composite IPY of the entire lending space is shown below for the last one year. In general, each asset listed on a lending protocol has its own market and terms for loans. Data from each cryptocurrency / asset listed by a protocol is combined to arrive at its composite IPY.

We can see from below that the overall IPY in the last year has increased starting from around $70M to currently standing at $885M. Around July the IPY fell considerably possibly due to the crypto market downturn, still it was able to stay above $500M. The IPY since the downturn appears to have rebounded back, though one can infer that borrowing demand is correlated to the overall crypto market cycles.

As far as individual protocol’s IPY is concerned, Aave appears to take the lead on this metric too. It generates almost 2.5 times the IPY of Compound and almost 12 times the IPY of Maker. This implies that Aave is able to attract much more borrowing demand compared to the other two. It would be worth investigating the reasons for this. One possible reason could be that Aave allows borrowers to select a stable or variable interest rate, while Compound and Maker only have variable interest rate options. This introduces uncertainty in interest payment amounts both for borrowers and lenders. Other possible reasons could be better user experience and newly added features in Aave V2 as highlighted in this article.

Discussion

Users seem to be engaging with DeFi lending protocols for a variety of reasons. One of the motivations has been to receive participation rewards e.g. valuable, tradable governance tokens resulting in overall higher APY compared to traditional lending. By guaranteeing IOU tokens’ redeemability, DeFi lending protocols also ensure full transferability and exchangeability of debt holdings.

Sophisticated investors as well as institutional investors leverage DeFi lending for trading. For example, an investor bullish on ETH may borrow, say, DAI to buy some ETH. In expectation of a price increase of ETH, investor would swap borrowed DAI for ETH on an exchange, hoping that the purchased ETH can be worth more DAI in the future to such an extent that it exceeds the loan amount and leaves the investor some profit. Similar to the borrow spiral discussed above, an investor can repetitively (i) borrow DAI, (ii) swap DAI for ETH, (iii) re-deposit borrowed ETH as collateral, (iv) borrow more DAI. As such, a “leveraging spiral” is formed to maximize the investor’s long exposure to a crypto-asset that is expected to appreciate.

Flash loans have opened up a huge space for innovation in arbitrage and to unlock collateralized borrow positions on lending protocols, however they can also be used for malicious actions e.g. in case of governance voting.

It is important to highlight that competing blockchains and overcollaterization problems may stifle growth of DeFi lending. Several protocols such as Cosmos, Polkadot and Solana are rushing to kickstart DeFi ecosystems on their own platforms, this may pull some developers and liquidity away from Ethereum based DeFi systems. However healthy competition and increased interest just goes on to demonstrate the value in the potential of DeFi. But perhaps the biggest limitation of current DeFi systems is overcollateralization of crypto assets. This causes capital inefficiency. Further, it does not help the unbanked since without a crypto collateral, they cannot access capital.

Overcollaterization problem can be potentially resolved via a credible reputation/credit system in DeFi. With this approach, based on the credit history and other relevant parameters, loans can be provided to users that meet certain criteria. This would allow for financial inclusion and induce more liquidity in the market to serve user needs.

Conclusion

Decentralized lending has enabled borrowers and lenders to earn yield and maximise their returns on investment on their crypto holdings, without needing to go through any centralised intermediaries. Though the current DeFi lendings’ offer exceptional yields (which are partly there to fuel adoption), it is unlikely these yields will be sustainable. However, billions of dollars worth of value locked, institutional interest and the increasing network effects make it likely that the DeFi lending platforms will continue to grow and offer acceptable yields to its users.

CURVE FINANCE: Let's Take A Curve Into Defi Of Stablecoins

Introduction

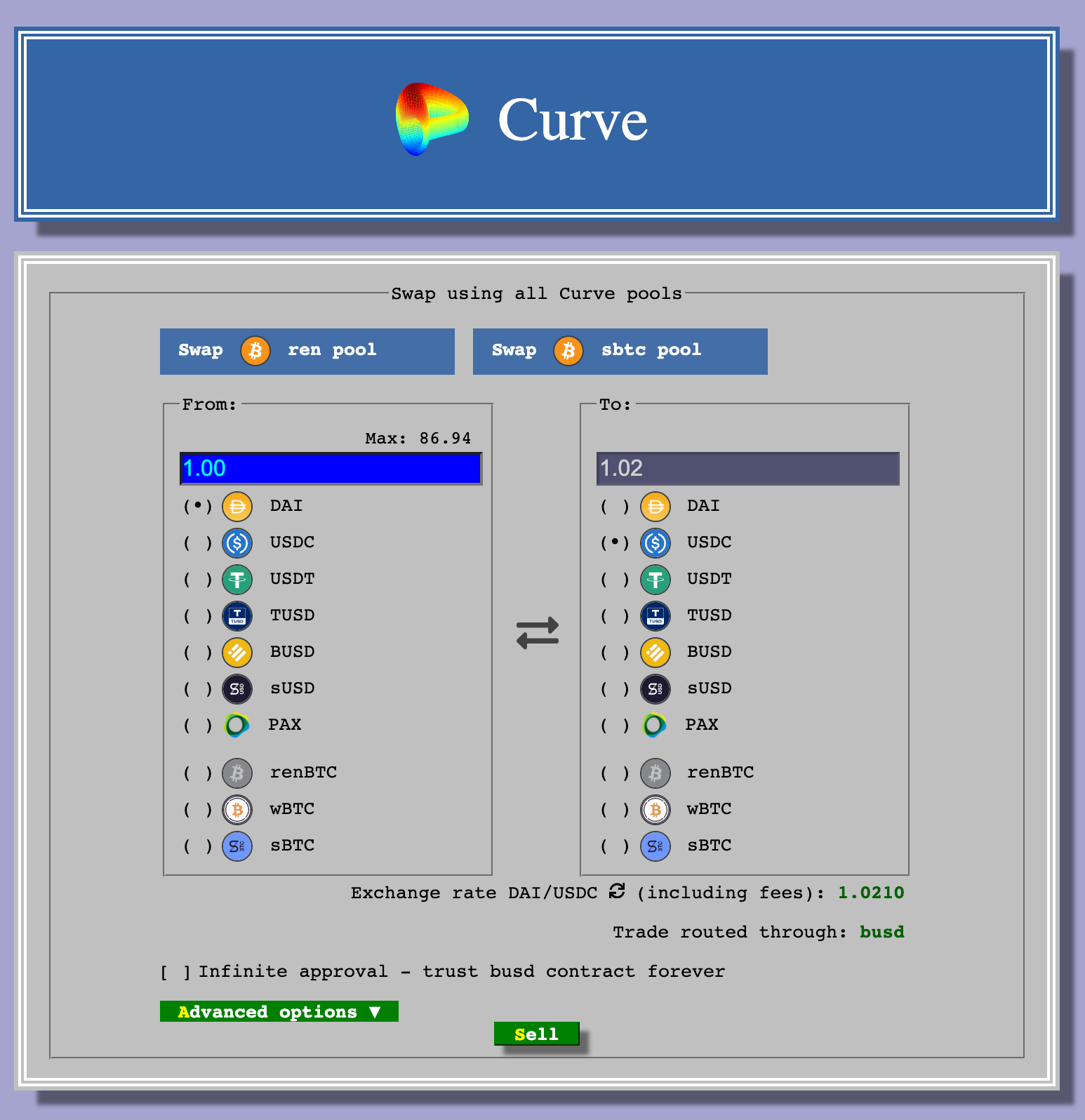

Curve finance is a decentralized exchange that facilitates the swapping of crypto-tokens. But it is specifically designed for stablecoins like DAI or USDT with low slippage and low transaction fee while using the liquidity pools like those of Uniswap. Let’s back up a little and first clear the basics.

Decentralized Exchanges

Let’s say Alice wants to send money to Bob. She can transfer the assets by going to a bank. Here a bank works as a centralized entity and verifies the transfer but cryptocurrencies are known for being decentralized.

In a decentralized environment, Alice can send Bob assets without the need of a central entity, and a set of independent nodes to verify the transfer.

Liquidity is the process where liquidity providers pour in their crypto tokens in a pool and allows others to exchange the tokens. They earn a fee on every swap where slippage is the price change of a token during a transaction.

Understanding this formula is extremely important as it is widely used in the decentralized exchange world to determine the price of two tokens in a particular pool. The variables x and y in the formula represent the quantities of two tokens and k being the constant. If the value of one token increases the value of the second token automatically decreases in order to maintain the constant k. However, this formula could be problematic when dealing with stablecoins as the stablecoins should remain constant. Also, while dealing with different flavors of the same tokens, prices have to be the same for each flavor.

Graph

What is Curve Finance?

The curve finance is a platform for the exchange of tokens rather particularly famous for stable tokens. Stable tokens are tokens whose value does not fluctuate rather remain stable.

It offers different flavors of similar tokens like ETH and BTC while using a formula called the STABLE-SWAP INVARIANT for swapping. The flat line in the graph ensures the stable swap of two coins. Uniswap uses the x * y = k formula where one token’s price can grow exponentially and the other token can lose its price and the two tokens could be dollars to pennies. Curve introduced the Stable-swap invariant in which both the tokens tend to remain stable.

Explanation

Let’s understand this with the help of an example:

Suppose, Uniswap pool has a pair of USDT/DAI, both of which are of $1 with a proportion of 50/50. After some swapping the pool becomes unstable now with a proportion of 60/40. Now we have an excess of USDT and a scarcity of DAI. So, the price of USDT will become slightly less than 1$ (0.97$) and DAI will become slightly more expensive than 1$ (1.03$) and the pool becomes lopsided. Here, Curve will incentivize the liquidity providers to pour in DAI thus making the pool stable. The formula handling this is known as the Stable-Swap Invariant.

This is what the Stable-Swap Invariant looks like:

Curve’s Growth

Stablecoins have become an integral part of De-fi with more and more varieties of stablecoins in the market. Which means that there is a bigger space for people trading stablecoins. The curve has captured the market and emerged to become a giant by offering low fees and slippage at the same time. Stablecoins on other exchanges might deviate from their price whereas Curve ensures stability, which is one of the many reasons behind Curve’s success.

Liquidity providers can earn rewards by providing liquidity in Curve pools just like Uniswap. Additionally, there is another way liquidity providers can earn extra rewards; by the concept of lending. Curve finance offers lending pools where liquidity providers can lend tokens to other exchanges like Compound. This takes place in the background and liquidity providers earn fees on top of the transaction fee, as some protocols enable lending and borrowing functionality to the users.

It’s important to note that the rewards are based on the transaction volume; they can be high or low.

You might be wondering about the security risks that might occur while lending a token to another exchange. Curve solves this issue by wrapping the token as a cToken(wrapped token) and lending it to Compound while backing the cToken to the original token.

With Curve, we can have a pool of three or four tokens as well.

Once you deposit the tokens in, you can split it among all the tokens in the pool or you can add just one token. After adding tokens to the pool you will get LP tokens. These LP tokens represent your share in the pool which can be used to stake and mine new CRV tokens.

The 3Pool is a pool with 3 tokens DAI, USDC and USDT, it does not matter in what token the user adds the liquidity as the reward generated is the same. You can get the LP tokens in all the tokens or in a single token.

A metapool is a pool where a stablecoin is paired against an LP token from another pool. For example, a liquidity provider can deposit DAI into 3Pool and earn pools liquidity token 3CRV.

Source: https://curve.fi/

CRV Token

CRV is Curve’s native token, which is generated when the user deposits and stakes the tokens on the Curve platform. It is awarded to liquidity providers, proportional to their share from the yields created by their pools. With Curve’s transition to become a DAO, CRV tokens also represent the holders’ rights to take part in its governance mechanism. That way they can make proposals and vote on them with CRV. Their Governance follows a ‘time-weighted’ voting system which simply means that the longer they hold CRVs, the greater their voting power in the DAO becomes.

Conclusion

Curve’s smart contract is audited by Trail of Bits but this doesn’t eliminate risks completely. Curve lends tokens to other exchanges and hence opens up another front to security risks. Curve finance is in the market for around a year and needless to say that hackers for sure have tried their unsuccessful attempts to steal the funds.

Decentralized finance (Defi) is arguably the most promising application of Ethereum blockchain, and Compound Defi protocol is taking advantage of this potential. With Defi services, users are granted access to multiple financial services that were previously offered by banks and other traditional institutions. Defi platforms like Compound leverage the features of smart contracts to offer accessible decentralized alternatives. This is the reason, it often refers as open finance. Some of the best-known uses cases of decentralized finance include lending protocols, decentralized exchanges, stable coins, and payment networks.

In traditional banks, once you have deposited your money, you can only earn interest but cannot use the money in any other way. Think about a situation where you can spend the money on your savings while still saving the money. This is exactly what Defi is trying to offer to its users. Compound Defi protocol is one of the companies working on providing such services. In this article, we will explore how this Ethereum based project is trying to allow people access to their savings.

What Is Compound Defi Protocol

Compound Defi protocol is a lending protocol that runs on the Ethereum blockchain. It is a pooled algorithm money market protocol. Like other Decentralized Finance (Defi) protocols, Compound Defi protocol is a network that is an open-source smart contract.

The focus of the Compound is to allow borrowers to access loans and lenders to provide loans. The Compound is able to achieve this by locking their crypto assets into the protocol. Each crypto-asset determines the demines the interest rate. Every mined block generates an interest. Borrowers can pay back the loan at any time, while assets can also be withdrawn in the same manner.

The Compound decentralized fiancé protocol also has a native token (cToken) that allows users to earn interest on their money. Users can also transfer, trade, and use the money in other applications. On the surface, you may think that the Compound is completely designed like other Defi protocols. The Compound protocol differs in the tokenization of assets locked in the system. We will talk about the cToken later on in this article. The Compound protocol is completely open; hence there is no need for any paperwork or intermediary.

If you have an Ethereum-enabled wallet, you can be part of the Compound market. The Compound provides users with three main services:

Compound provides liquidity

It helps users to avoid credit risk, and

Compound frequently adjusts interest rates based on the demand and supply of crypto assets.

As a market player on Compound, you are not guaranteed a fixed interest because there is no duration to your participation. As a lender or borrower on the platform, you can only know what the interest rate is at that moment. The interest rate can change at any point. The design of the Compound protocol ensures that there is no counterparty risk. However, it would be best if you didn’t forget that there is also the risk of code vulnerabilities.

The Interest Rates On Compound Defi Protocol

When we consider the interest rates on the Compound, we will undoubtedly see an interesting pattern. On the platform, it is obvious to see that it is attractive to supply Dai, Sai, or USDC stable coins compared to other crypto assets. By supplying Dai, you could earn an interest of up to 8% every year. This is contrary to the paltry 0.01% interest you earn when you supply Ethereum. It is glaringly to us that stable assets are the most desirable assets to supply on the Compound protocol. If you borrow volatile assets on the Compound protocol, the amount you will have to repay becomes more uncertain. Therefore, you will have to consider both the unstable interest rates and the volatile value of the crypto asset. Hence, making a prediction on your repayment would be very tricky, if not difficult.

The Compound Native Token (cToken)

The Compound tokens (cToken) are ERC-20 tokens that represent a user’s fund deposit on the Compound protocol. When a user puts another ERC-20 coin like the USDC in the protocol, the user gets an equivalent amount of cTokens. For instance, when you lock up USDC in the protocol, it generates cUSD tokens. These cUSD tokens automatically earn interest for you. Whenever you want, you can redeem your cUSDC for the normal USDC, including the interest paid in USDC. The cTokens act as twins of the original Compound token. When a user supplies Dai or any other crypto assets to the Compound protocol, their balance will be represented in cTokens. This is how the interest rates are calculated on the Compound Defi protocol. For example, when Dai gets supplied to the Compound protocol, the wallet is represented in cDai. Meanwhile, the interest is represented by the Dai token, which increases in price relative to Dai. All the received Dai tokens will be pooled together by the Compound’s smart contract. Over time, the exchange rate between cDai and Dai increases, just as the total borrowing balance also increases. When a user withdraws his/her balance from the Compound protocol, the process automatically converts cDai into Dai at the current rate. This transaction also includes the additional interest rate. The cTokens always appreciate their counterparts.

The Compound Governance

Although Defi implies that there is no single point of failure, however, that is not practically the case, all decentralized finance (Defi) projects are developed by companies who also retain full control of the smart contract development. By a simple flip of a switch, the entire protocol can be turned off, and the Compound is not excluded. The idea behind such a scenario is to have failsafe in situations like unexpected blockchain forks, black swan events, and smart contract hacks. However, Defi with all its highlighted flaws is far better than traditional financial institutions. Recently, Compound announced the release of a new governance token (COMP), which aims to remove the largest point of failure in the protocol. The Compound team is seen as the largest point of failure in the system, and anyone with at least 1% of the total COMP token can vote for proposals. These proposals are executable code that is subject to a three-day voting period.

Borrowing On Compound Defi Protocol

The fact that Compound aims to have a zero counterparty risk means that borrowers will have to deposit collateral before borrowing from Compound. The ability to maintain excess collateral ensures that there is a near-zero chance of a borrower defaulting with payment. For example, if you want to borrow Dai, you will have to deposit ETH as collateral. Each borrowing position is over collateralized; therefore, the value you borrow will be less than what you will deposit. Meanwhile, the underlying collateral is also volatile and could drop below a certain threshold. If it drops, the smart contract trigger will close the position (liquidation). In this instance, the borrower gets to keep the borrowed asset but loses the collateral. For a user to get back his/her collateral, the user will have to repay the credit, and that includes the outstanding interest.

Lending on Compound Defi Protocol

It is akin to a typical cash account where you earn by leaving your money in the bank. In Compound, you will need to deposit your crypto asset before you can earn interest. You can withdraw your asset at any time since there is no duration lock, and you won’t get penalized.

Conclusion

Compound Defi protocol wants to help you have more control over the money you save and earn. Although the Compound project has its shortfalls, the long-term goal is to become completely decentralized.

Xord is a Blockchain development company providing Blockchain solutions to your business processes. Connect with us for your projects and free Blockchain consultation at https://blockapexlabs.com/contact/

Decentralized Finance Categories Explained

In this article, you will get to know about the Decentralized Finance categories and projects associated with each category.

Introduction:

Decentralized Finance (DeFi), is finance but on the blockchain. In simpler terms, DeFi is permissionless dealing with finance, meaning, the intermediary such as banks, insurance companies, brokers, and more in real finance are replaced by smart contracts in Ethereum.

DeFi projects fall into different categories, these categories are:

Lending:

In Centralized Finance (CeFi), lending is when you allow someone or an organization to utilize assets by borrowing and paying it back later on. The Decentralized Finance categories also include lending, which is not that different. In DeFi, as the name suggests, the assets are cryptocurrencies or tokens, with no central authorities. Lending protocols allow the lender to earn interest as an incentive.

In the traditional finance system, you have to give proof of your identity in order to take out a loan. DeFi removes all of this friction. The collateral amount is all you need to take out a loan, there is no need for proof of identity.

The number of tokens or cryptocurrencies you can take out as a loan varies depending upon the rate of that token or cryptocurrency. At times, the amount of collateral put is greater than the loan.

A new lending protocol lets you borrow money without submitting collateral, i.e. via flash loans.

Flash loans or zero risk loans are contracts lending money. But there is one catch, it has to be paid back by the end of the execution of the same transaction. If he or she fails to do so the whole transaction will be reverted as if it never happened. This is only possible in the blockchain. The interest in flash loans is either zero or nominal.

Projects:

Some of the leading Decentralized Finance lending projects are:

Decentralized Finance categories also include DEXes, which deals with the exchange or trading of cryptocurrencies or tokens. Being part of the blockchain there is no need for a central authority. As a result, DEXes don’t have one point of failure. Your cryptocurrencies or tokens stay in your wallet, hence it reduces the number of risks. You are not putting your assets under someone else’s control, like in centralized exchanges where you put your assets in the exchange. The only time your assets leave your wallet is when a transaction takes place. DEXes don’t require some long procedure to verify your identity and provide legal documentation, as long as you have assets, you can trade them without restrictions. Smart contracts help to make all of these features possible.

DEXes use the concept of either order books or liquidity pools.

Using Order Books:

Order books are essentially just books with trade orders in it. The process of using order books is as below.

Users willing to exchange submit a buy or sell request, this request is stored in order books. This ordering turns the user into a “maker”.

These order books hold records about which tokens the user is willing to exchange and for what in return.

To validate the order, makers sign it with the private key.

This order is broadcasted through the exchange network and takers come forward with a trade.

If the maker is satisfied they confirm the order, and the smart contract takes care of the rest of the process.

Using Liquidity Pools:

The problem with order books is that they bring back the obstacle of centralization.

Decentralized Finance projects jump over this obstacle with the help of liquidity pools. The market makers are referred to as liquidity providers in this model.

Let’s look into how liquidity pools work.

Take a simple pool, this pool holds two tokens, when a new liquidity pool is created, a liquidity provider supplies both tokens of equal value to the liquidity pool and sets their initial price. Every person adding tokens to the liquidity pool will provide an equal value of both tokens. Liquidity providers earn LP tokens, based on how much liquidity they provide to the pool, when a trade takes place, a fee value is distributed among all LP token holders. With each trade, the deterministic price algorithm adjusts the price of the tokens. This mechanism is known as Automated Market Making.

Derivatives are contracts with their values based on something else. By definition,

"The derivative itself is a contract between two or more parties, and the derivative derives its price from fluctuations in the underlying asset” - Investopedia.

To understand derivatives completely, let’s consider an example:

When the price of wheat increases, the price of bread will increase, similarly when the price of wheat decreases, the price of bread will decrease. Now, a wheat seller will have an advantage when the price of wheat increases whereas a bread seller will be at a disadvantage. The opposite is true when the price of wheat decreases. Suppose, the wheat seller estimated that the price of wheat will decrease, and the bread seller estimated that the price of wheat will increase in the future. So they enter into a contract that regardless of the price of wheat in the future, for a specified period, they will make the trade at a certain fixed price. This is derivative in finance.

Now you must be thinking that if these people wouldn’t have signed the contract, one of them would have earned more. It’s true, however, both the parties saw risk and minimized it.

In DeFi, derivatives are the same as in CeFi.

The prices of cryptocurrencies are volatile, hence derivatives make great use in DeFi.

Synthetic Assets:

The values of assets fluctuate in both CeFi and DeFi, If you think about today’s financial markets, there are things you can buy or sell in one area or country. Let’s take gold or shares as an example, the local legal infrastructure makes it hard or impossible to buy them. Synthetic assets make it possible, let’s say these shares or gold is represented by an ERC, you can buy that from anywhere through the internet. You don’t need to have a safe or a brokerage account.

Projects:

Some of the leading projects working on Decentralized Finance derivatives are:

In finance, payments refer to the transferring of assets or services in return for assets or services. In other words, payments are just transactions.

Transactions are plausibly the foundation of the blockchain, more specifically peer-to-peer transactions or payments. The idea behind DeFi payments is to facilitate the unbanked and underbanked population as well as institutions. Decentralized Finance payments are secure and direct.

Stablecoins are cryptocurrencies that provide stability to the prices of cryptocurrencies. As you know the price of cryptocurrencies is volatile. Collateral is deposited in the smart contracts and then a portion of the value of those deposited collateral is paid out as a newly minted stablecoin. Of course, these can be traded like any other cryptocurrency. This collateral can be a commodity, a fiat asset, or some other cryptocurrency.

Decentralized Finance categories also cover Insurance. Insurance is a safety net. The company provides compensation or reimbursement for specified loss, fraud, or accidents. DeFi is still emerging and may contain faults or bugs or is even prone to hack attacks, many examples of exploitation occurred this very year. The assurance that in such a case, you will be compensated was much needed. People are still hesitant to invest large amounts in DeFi projects, with insurance projects coming forward, DeFi will have the opportunity to grow further.

Indexing, in finance, is the statistical change in market or stocks. Consider it a basket of stocks measured together, for example, the FTSE 100 index represents 100 major companies listed on the London stock exchange. The rise or fall of stock’s rate of the companies listed on this index has the same effect on the index. Indices can be country-based, or they could be the exchange-based they are listed on, then there are regional indices. Index funds are funds that track a market’s index. This market can be a market of stock, bonds, currencies, commodities, or other assets.

In simple terms index funds are buying shares with funds. In DeFi, it is the same. Then a market expert invests this money or funds to buy cryptocurrencies, you don’t have to keep track of risks, calculate returns. An index fund does all of this for you. But DeFi Index funds are more suitable for long runs. Index funds give the advantage of simplified investing without having to worry about maintaining a portfolio.

CeFi came into existence much earlier than DeFi, so while Decentralized Finance categories are similar to Centralized Finance, it is still emerging. DeFi is one of the greatest uses of blockchain and in the near future we will get to see more applications of DeFi.

DeFi projects are dominating the blockchain markets, a total of $9.06B USD are locked in DeFi projects as of 18th September 2020. Uniswap dominates the market by holding 15.52% of the market.

Xord is a Blockchain development company providing Blockchain solutions to your business processes. Connect with us for your projects and free Blockchain consultation at https://blockapexlabs.com/contact/

Decentralized Finance — Financial Enabler of the Future

Decentralized Finance

The invention of Blockchain has resonated several solutions; one such solution is cryptocurrency, and they have paved ways for many ways of doing things, including banking. Initially, space had limited or restricted adoption, but thanks to the recent use cases and applications of Blockchain and cryptocurrency like Decentralized Finance and DApp, among others that brought several use cases to space.

First, it was the Initial Coin Offering (ICO), that aims to deepen cryptocurrency and Blockchain adoption in general. As soon as the ICO era was becoming somehow obsolete, Decentralized Finance (DeFi) took the lead.

DeFi is the financial enabler of the future. It uses emerging technologies like Blockchain, Yield farming, internet, etc. to bring financial inclusion. In other words, it is an open financial movement that breaks the barrier of the centralized system hence broadly known as Open Finance.

However, before diving deep, here is a simplified definition of DeFi, according to Binance Academy:

“The movement promotes the use of decentralized networks and open-source software to create multiple types of financial services and products. The idea is to develop and operate financial dApps on top of a transparent and trustless framework, such as permissionless blockchains and other peer-to-peer (P2P) protocols.”

DeFi and Traditional Banking

Decentralized Finance bridges the gap between the banking system and the average user. It tries to decentralize and distribute banking among users and take banking decisions away from central parties. Usually, there are bureaucracies in traditional banking. However, Decentralized Finance protocols are promising to lift them. Consequently, you will get to appreciate the distinctions of DeFi to conventional banking with the following points:

Digitalize Assets

Digital assets holders are deprived of making transactions in traditional banking, simply because of trust and other constraints. However, the Decentralized Finance assures digital asset inclusion, where users and holders alike can transact, invest, and own as needed. Meanwhile, digital assets include electronic, encrypted, and distributed money. For instance, the DeFi gives a cryptocurrency holder access to banking.

Transparent

Since the underlying technologies of DeFi combine a trustless, transparent, and secured system, transactions on DeFi are transparent and are recorded on a Blockchain. It restores the broken link of transparency in the system.

Interoperable

If you have tried building applications or even performing some transactions through the traditional system, you may either be limited or have several compatibility issues. However, the DeFi protocols built on dApps are designed mainly as open sources for users to perform services of choice. That said, a user who wants to save, loan, lend, stake, etc., can interchangeably do that without filing documents and possibly seeking approvals from the management.

Global access

DeFi platforms operate decentralized applications (dApps). Therefore, they provide access to everyone who has access to the internet. Also, the underlying technology of DeFi, Blockchain, makes it easy for everyone across the globe to connect to the dApp.

Concurrently, unlike the traditional banking systems where you require a third party for access when the need arises, DeFi solves that for you.

Moreso, the more you require third parties to gain access to the platform, you have to pay some fees, therefore, since there is no such barrier in DeFi, you have no such fee to consider.

Distributed and Permissionless

There are permissioned, public, private, and permissionless Blockchain distributed ledger models network depending on the use case, the DeFi are designed as permissionless. Usually, the type of distributed ledger, a single ledger system that shows the transactions in a timestamp manner, is designed to suit the use case. Therefore, the DeFi operates a permissionless and distributed ledger model where users only need to follow the Smart Contract’s terms to perform transactions.

Meanwhile, the Smart Contract functionalities of DeFi is a Blockchain protocol that automates deals, negotiation, and agreements between parties. Consequently, it helps the DeFi community to self bank upon reaching the terms enshrined in the contract. Contrary to the traditional system where users may be panicking if there is a failure to fulfill agreements, the Smart Contract reverses the deals once agreements are not met.

Also read our latest article on the Polkadot Blockchain network here.

Uses and Applications of DeFi

Like every other invention of Blockchain, Open Finance has several and increasing numbers of use cases. However, let’s start by looking at the functions of Decentralized Finance.

In a holistic view, the functions of DeFi include;

Creating a monetary banking system

Peer to Peer networks for trustless transactions

Deploying financial instruments to further provide liquidity, market making, and overall financial inclusion.

However, the various functions created opportunities for various types of DeFi services; funding protocols, software development tools, index construction, subscription payment protocols, data analysis applications, KYC, AML, and other identity management services. Nonetheless, the following use cases manifests the various functions and types of DeFi services:

Borrowing and Lending

Some people mistake decentralized borrowing and lending. However, borrowing refers to getting loans while lending is making a deposit for interest or issuing out loans.

Before Decentralized Finance, borrowers and lenders approach third parties to sign or fill some documents which may not be transparent. Consequently, the Open Financial movement enabled the parties; borrowers, and lenders to transact

Stablecoin and Decentralized Reserve

Since the cryptocurrency assets are largely volatile, stable coin and the decentralized reserve is a way of balancing the price fluctuations. They are achieved by pegging digital assets to a basket of currencies or goods, unlike Bitcoin, Ethereum, among others that are not pegged on anything. For instance, MakerDao, WBTC, and others enabled asset-backed cryptocurrencies to reduce price swings and market uncertainties.

Therefore, a stablecoin somehow makes crypto legitimate as it draws the attention of the states who are currently developing or researching Central Bank Digital Currencies.

Savings

Before now, if you want to save money, you’d find a bank to save. However, you may no longer bother looking for a central party to deposit your money to save. Therefore, you can simply save through a decentralized saving platform. Therein, you only need to deposit once you agree to the terms and conditions and the interest rate within a stipulated time. Consequently, you have your keys to finance through Open Finance. Concurrently, most stablecoin offering platforms offer to save including, Dia, Gemini Dollar, and WBTC among others.

Automated Token Exchange

One of the applications of Open Finance is to automate trades and enable market making. Therefore, it does that through a mechanism called “Automated Token Exchange”.

Consequently, it uses an innovative mechanism known as Automated Market Making to automatically settle trades near the market price and allow users to provide liquidity to the market. While there are several projects automating trades and offering liquidity, Uniswap is the most popular one. However, other decentralized exchanges are offering the same. They include but not limited to; AirSwap, Bancor, Kyber, IDEX, Paradex, and Radar Relay.

Decentralized Marketplace

These applications of DeFi enable financial innovations. For instance, decentralized exchanges, synthetic assets, decentralized prediction markets, and many more. Contrary to the centralized marketplaces, it simplifies digital assets trading between users across the nodes without the need for a third party or central control system.

It hosts decentralized protocols that match trades and improves liquidity, tokenization, and other things that make decentralized trading work. Concurrently, Bisq, Airswap Protocol, IDEX, Bancor, Kyber Network, Uniswap, and Binance DEX among others, are examples of the DeFi decentralized market use cases.

Conclusion

According to Coingecko, DeFi Coin and DEX, is currently $14B, $451M market cap, and trading volume respectively. Therefore, it could be inferred that the market is new and has rapid growth potential. Consequently, it is a statement of fact that DeFi is the future of finance. However, it can achieve that in a matter of time and only when individuals have full access to self-banking.

Xord helps businesses build reliance by integrating Blockchain with business processes. Get in touch with our Blockchain experts for projects and consultation: https://https://blockapexlabs.com/contact/